States like Kansas that are struggling to balance budgets could use school choice programs as a way to save money.

When states consider implementing school choice programs, a common objection is that the state can’t afford school choice. Public school spending interest groups will tell legislators that school choice programs drain money from already under-funded public schools. School choice, they will say, is a luxury the state can’t afford, much less local school districts.

Research shows, however, that school choice programs can be constructed in a way that does not harm local school districts. Simply: A typical Kansas school district has variable costs of $8,709 per student. If such a district loses a student and associated funding, as long as that funding is less than $8,709, the district’s fiscal situation is improved. Base state aid in Kansas is $3,852, although state spending per student is $7,088 (2013 to 2014 school year). So it’s quite likely that any student who leaves a public school for any reason, including attending a private school or home school, improves the fiscal standing of the district, on a per student basis.

At the state level, a similar dynamic applies, although the reasoning is easier to follow: If the state funds that follow the child are less than average state spending per student, the state has the opportunity to save. The savings can be large, if states are willing to embrace choice programs.

Savings from school voucher programs, from Friedman Foundation for Educational Choice. Click for larger version.In the report The School Voucher Audit: Do Publicly Funded Private School Choice Programs Save Money?, prepared for the Friedman Foundation for Educational Choice, the author finds that from 1991 to 2011, voucher programs alone have saved state governments a cumulative $1.7 billion. While representing just a small portion of total state spending, this total is from the ten states that had voucher programs in effect at the time of the study. In 2011 about 70,000 students were in these voucher programs.

The key understanding is that when student enrollment declines — for whatever reason — schools see reduced costs. For those who deny that, there is a corollary:

Opponents claim, simplistically, that school choice drains money from the public school system. That rhetoric obscures an important fact: A public school is also relieved of a cost burden for any student switching to private school. By not acknowledging such variable cost savings, opponents implicitly argue that all public school costs are “fixed.” By extension, they then conclude that the loss of funding for a student using a voucher to transfer to a private school harms all the remaining students at the affected public school. But that argument strains credulity: If there were no savings when a public school’s enrollment declines, logic dictates there would be no additional costs for schools when their enrollment grows.

It may be that costs do not decrease (or rise) smoothly as enrollment declines: “That phenomenon reflects the reality that schools must fund classrooms, not students.” Many businesses face this cost structure and are able to adapt, and it should be no different for schools.

An important note is that as students leave a school and its cost burden falls, the school must actually take steps to reduce spending in response to the reduced cost burden it experiences.

A problem is that critics of school choice may notice that no money has been saved after school choice programs are implemented. This is because “savings are typically reallocated to other spending, either directly or indirectly.” It is not uncommon for public schools to be held fiscally harmless for declining enrollments. The net effect is that public schools are paid for students that are no longer enrolled, and that absorbs the savings due to school choice. The cost savings are there; but are still spent on schools rather than spent elsewhere, saved, or returned to taxpayers.

This month, parents and children from around Kansas rallied in the Kansas Capitol for school choice.

Speakers included James Franko of Kansas Policy Institute. He told the audience that children deserve better than what they are getting today. For many, he said that might be in a public school, but for many others it may be in a private school. Parents and their children should make that decision. It shouldn’t be based on their zip code. Individuals, not institutions, should be the focus.

Kansas now has a private school choice program. Franko told the audience that newspaper coverage of this program emphasizes how it helps private schools and hurts public schools. But we should be reading stories about how school choice helps kids, giving each child the freedom and opportunity to find the best educational fit. He explained that school choice also helps the students who remain in public schools, referring to a Friedman Foundation for Education Choice study. “It’s about helping every single child,” he said.

The study Franko mentioned is A Win-Win Solution: The Empirical Evidence on School Choice. In its executive summary, author Greg Forster, Ph.D. writes “Opponents frequently claim school choice does not benefit participants, hurts public schools, costs taxpayers, facilitates segregation, and even undermines democracy. However, the empirical evidence consistently shows that choice improves academic outcomes for participants and public schools, saves taxpayer money, moves students into more integrated classrooms, and strengthens the shared civic values and practices essential to American democracy.”

Later, the specific finding that Franko used in his talk: “Twenty-three empirical studies (including all methods) have examined school choice’s impact on academic outcomes in public schools. Of these, 22 find that choice improves public schools and one finds no visible impact. No empirical study has found that choice harms public schools.”

Michael Chartier of the Friedman Foundation for Education Choice said that there are now 51 school choice programs in 24 states plus the District of Columbia.

Andrea Hillebert, principal of Mater Dei Catholic School in Topeka told the audience that school choice benefits families, schools, and the state. Families can choose the learning environment that is best for their children, and are not penalized if they choose a school that is not run by the government. She told the audience that “school choice encourages — requires — families to take an active role in shaping their students’ future.” Schools benefit because consumer choice is a catalyst for innovating programming and continuous improvement. The state benefits from the increased achievement of students in non-public schools.

Susan Estes of Americans for Prosperity – Kansas explained that even as a former public schoolteacher, it has been a challenge for her to navigate the school system so that the needs of her three children were met. She said that parents not only deserve, but have the right to be the primary decision maker for their children.

Bishop Wade Moore, founder and principal of Urban Preparatory Academy in Wichita, completed the program. Urban Prep is a new private school in northeast Wichita, and students from that school attended the rally. He said that our legislators have “a moral responsibility to do what is right for each Kansas kid.” He mentioned the students that are pushed through the system until they graduate, but are unprepared for college, trade school, or employment. “A lot of those children have no chance at life. So we say that we have a crisis in this nation,” he said.

Alluding to how Kansas has few school choice programs, Moore said “It’s time for us to wake up and move ahead, like the rest of the nation, in education reform.” He said that he heard a school superintendent make the statement that our children and parents have a choice in education. He said “They can choose one of our schools to attend.” That is not choice, Moore said. Real choice is when parents have the opportunity to go outside the public school system.

The reason for the poor academic performance of many children is that their parents have not had choice and control over the children’s education. “It is imperative that all children, regardless of their race, gender, place of residence, and socio-economic status, learn the concepts and strategies necessary for them to develop and succeed,” he told the audience.

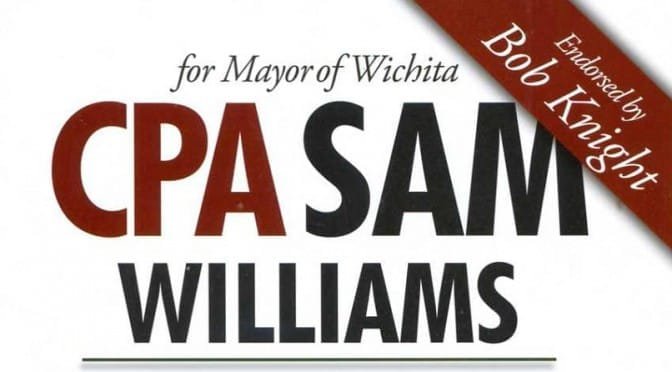

Sam Williams, a candidate for Wichita mayor, is not entitled to use the title “CPA,” according to Kansas law.

“I am a Certified Public Accountant.”

“– Sam Williams, CPA”

“CPA Sam Williams”

“Being a CPA, Sam Williams …”

“Bert Denny, CPA — Treasurer”

Sam Williams campaign mailer.These are some of the statements you’ll find on campaign and biographical material for Wichita mayoral candidate Sam Williams. But he isn’t licensed as a CPA, and Kansas law is clear on who can use the title “CPA.”

Kansas law states: “It is unlawful for any person, except the holder of a valid certificate or practice privilege pursuant to K.S.A. 1-322, and amendments thereto, to use or assume the title ‘certified public accountant’ or to use the abbreviation CPA …”

When asked if he was a licensed CPA in Kansas, Williams said that he was certified, but doesn’t have a license to practice. Asked about the statute that regulates unlawful use of the title “CPA,” Williams said “I never heard that before.”

It’s understandable that Williams does not have a CPA license in Kansas. He had such a license in Utah, expiring in 1990. In Wichita he worked as an executive in the advertising industry. He was not offering accounting services to the public.

Sam Williams campaign mailer.

As candidate for mayor of Wichita, the title “CPA” is front and center in Williams’ campaign. Advertising pieces make frequent use of the title, promoting business-related qualifications like knowing how to balance a budget and minimizing taxes.

We might dismiss this use of the CPA title as the type of resume-burnishing that is routine for candidates, and perhaps for anyone looking for a job. But Kansas has a law.

It’s not an obscure law, as this issue has been in the news. Last year United States Representative Lynn Jenkins of Topeka was granted special treatment by the Kansas Board of Accountancy, allowing her to continue to use the title “CPA” even though her license had expired. This was widely reported, and the Wichita Eagleeditorialized on this issue, quoting a Nebraska accounting board official as saying “She’s misleading the public.”

Sam Williams knew of the Jenkins case. He mentioned her by name when asked about using the “CPA” title. He knew of the controversy.

Of note, Williams’ treasurer is a CPA.

The Kansas statute

A Kansas law, K.S.A. 1-316 (c), states “It is unlawful for any person, except the holder of a valid certificate or practice privilege pursuant to K.S.A. 1-322, and amendments thereto, to use or assume the title ‘certified public accountant’ or to use the abbreviation CPA or any other title, designation, words, letters, abbreviation, sign, card or device likely to be confused with ‘certified public accountant.’”

A violation of this law is a misdemeanor, carrying a fine of up to $5,000 and up to one year imprisonment, or both.

Inquiry to the Kansas Board of Accountancy finds that Sam Williams has never had a CPA certificate in Kansas. His certificate from Utah expired in 1990, about the time Williams moved from Utah to Kansas.

While the statue seems clear, additional information from the Kansas Board of Accountancy is less than clear. In a document titled Who may use the CPA title in Kansas?, holds this advice; “For instance — if the CPA is a controller, CFO or an employee of a company that is not a CPA firm, whose responsibilities are to his/her employer only, then the use of CPA is allowable if used with the person’s name, the name of the company, and the person’s position with the company.”

This seems to allow someone like Williams — who was an executive with an advertising agency until retiring last year — some latitude in the use of the CPA title.

But the same document holds this: “What is also not allowed without a valid permit to practice, is advertising, phone book listing, letterhead, signature as a CPA on documents provided to the public (this includes friends and family), or third parties relying on the information provided.”

But recent history shows that when cash is needed, local governments have responded positively.

When Hawker Beechcraft threatened to leave Wichita for Baton Rouge, Wichita and Sedgwick County contributed $2.5 million each for an incentive. (Never mind that the threat to move was not real.)

Not long after that, the city and county contributed $1 million each for an incentive for Bombardier Learjet.

So there is recent history that shows when officials feel that spending on cash incentives is necessary, the city and county find the money. It’s difficult to imagine that if GWEDC officials had come to the city or county with a need for cash — especially if a deal was truly hinging on a cash contribution — that the council and commission would not find the money somewhere.

Job creation in context

For 2014, GWEDC claims credit for creating or retaining 424 jobs.

The Bureau of Labor Statistics tells us that for 2014, the labor force for local geographies was:

Wichita: 185,179

Sedgwick County: 242,460

Metro Wichita: 300,911

For each area, 424 jobs amounts to this percent of the labor force:

“Yes Wichita” campaign materialWhile economic development officials complain of lacking a deal closing fund, during last year’s sales tax campaign we were told that Wichita would not be competing by giving out cash. Material on the “Yes Wichita” campaign website, under the heading “Why is this plan different?” reads “It’s not about cash for jobs — it’s about investing in ourselves.”

Later on the same page: “We’ll let other cities compete with cash and instead we’ll invest in our people and infrastructure.”

A problem with wasteful spending in downtown Wichita is gradually curing itself, creating another problem in its place.

A bench at the heart of downtown Wichita should be illuminated at night by four lights. Only one light works, probably because the others have been left switched on 24 hours per day.

So wasteful spending on street lights during the day is being replaced by unlit streets at night.

What message does wasteful spending on street lights during the day send?

it’s difficult to show three nonfunctioning lights next to one that works, I’m afraid.Perhaps more importantly, what impression does nonfunctioning lights at night create — three of four at this bench? And at one of our major downtown intersections? Across the street from our nice boutique hotel?

Is this the “walkable” downtown we’re trying to create?

I suppose that Wichita city leaders want to be seen taking care of our larger problems, and of those, we have a few. But this long-running problem with lights at this downtown street side bench needs to be taken care of soon. Visitors to our town may not be aware of the lofty and sweeping rhetoric of our mayor, bureaucrats, and civic leaders.

In this episode of WichitaLiberty.TV: We’ll take a look at a few things Wichita Mayor Carl Brewer told the city in his recent State of the City Address. Then a look at topics from a new book titled “The Libertarian Mind: A Manifesto for Freedom.” View below, or click here to view at YouTube. Episode 76, broadcast February 22, 2015.

The Kansas STAR bonds program provides a mechanism for spending by autopilot, without specific appropriation by the legislature.

Under the State of Kansas STAR bonds program, cities sell bonds and turn over the proceeds to a developer of a project. As bond payments become due, incremental sales tax revenue make the payments.

STAR bonds in Kansas. Click for larger version.It’s only the increment in sales tax that is eligible to be diverted to bond payments. This increment is calculated by first determining a base level of sales for the district. Then, as new development comes online — or as sales rise at existing merchants — the increased sales tax over the base is diverted to pay the STAR bonds.

Often the STAR bonds district, before formation, is vacant land, and therefore has produced no sales tax revenue. Further, the district often has the same boundaries as the proposed development. Thus, advocates often argue that the bonds pay for themselves. Advocates often make the additional case that without the STAR bonds, there would be no development, and therefore no sales tax revenue. Diverting sales tax revenue back to the development really has no cost, they say, as nothing was going to happen but for the bonds.

This is not always the case, For a STAR bonds district in northeast Wichita, the time period used to determine the base level of sales tax was February 2011 through January 2012. A new Cabela’s store opened in March 2012, and it’s located in the boundaries of STAR bonds district, even though it is not part of the new development. Since Cabela’s sales during the period used to calculate the base period was $0, the store’s entire sales tax collections will be used to benefit the STAR bonds developer.

(There are a few minor exceptions, such as the special CID tax Cabela’s collects for its own benefit.)

Which begs the question: Why is the Cabela’s store included in the boundaries of the STAR bonds district?

With sales estimated at $35 million per year at this Cabela’s store, the state has been receiving around $2 million per year in sales tax from it. But after the STAR bonds are sold, that money won’t be flowing to the state. Instead, it will be used to pay off bonds that benefit the STAR bond project’s developer — the project across the street.

Taxation for public or private benefit? STAR bonds should be opposed as they turn over taxation to the private sector. We should look at taxation as a way for government to raise funds to pay for services that all people benefit from. An example is police and fire protection. Even people who are opposed to taxation rationalize paying taxes that way.

But STAR bonds turn tax policy over to the private sector for personal benefit. The money is collected under the pretense of government authority, but it is collected for the exclusive benefit of the owners of property in the STAR bonds district.

Citizens should be asking this: Why do we need taxation, if we excuse some from participating in the system?

Another question: In the words of the Kansas Department of Commerce, the STAR bonds program offers “municipalities the opportunity to issue bonds to finance the development of major commercial, entertainment and tourism areas and use the sales tax revenue generated by the development to pay off the bonds.” This description, while generally true, is not accurate. The northeast Wichita STAR bonds district includes much area beyond the borders of the proposed development, including a Super Target store, a new Cabela’s store, and much vacant ground that will probably be developed as retail. The increment in sales taxes from these stores — present and future — goes to the STAR bond developer. As we’ve seen, since the Cabela’s store did not exist during the time the base level of sales was determined, all of its sales count towards the increment.

STAR bonds versus capitalism In economic impact and effect, the STAR bonds program is a government spending program. Except: Like many spending programs implemented through the tax system, legislative appropriations are not required. No one has to vote to spend on a specific project. Can you imagine the legislature voting to grant $5 million per year to a proposed development in northeast Wichita? That doesn’t seem likely. Few members would want to withstand the scrutiny of having voted in favor of such blatant cronyism.

But under tax expenditure programs like STAR bonds, that’s exactly what happens — except for the legislative voting part, and the accountability that (sometimes) follows.

Government spending programs like STAR bonds are sold to legislators and city council members as jobs programs. Development and jobs, it is said, will not appear unless project developers receive incentives through these spending programs. Since no politician wants to be seen voting against jobs, many are susceptible to the seductive promise of jobs.

But often these same legislators are in favor of tax cuts to create jobs. This is the case in the Kansas House, where most Republican members voted to reducing the state’s income tax as a way of creating economic growth and jobs. On this issue, these members are correct.

But many of the same members voted in favor of tax expenditure programs like the STAR bonds program. These two positions cannot be reconciled. If government taxing and spending is bad, it is especially bad when part of tax expenditure programs like STAR bonds. And there’s plenty of evidence that government spending and taxation is a drag on the economy.

The word “capitalism” is used in two contradictory ways. Sometimes it’s used to mean the free market, or laissez faire. Other times it’s used to mean today’s government-guided economy. Logically, “capitalism” can’t be both things. Either markets are free or government controls them. We can’t have it both ways.

The truth is that we don’t have a free market — government regulation and management are pervasive — so it’s misleading to say that “capitalism” caused today’s problems. The free market is innocent.

But it’s fair to say that crony capitalism created the economic mess.

But wait, you may say: Isn’t business and free-market capitalism the same thing? Not at all. Here’s what Milton Friedman had to say: “There’s a widespread belief and common conception that somehow or other business and economics are the same, that those people who are in favor of a free market are also in favor of everything that big business does. And those of us who have defended a free market have, over a long period of time, become accustomed to being called apologists for big business. But nothing could be farther from the truth. There’s a real distinction between being in favor of free markets and being in favor of whatever business does.” (emphasis added.)

Friedman also knew very well of the discipline of free markets and how business will try to avoid it: “The great virtue of free enterprise is that it forces existing businesses to meet the test of the market continuously, to produce products that meet consumer demands at lowest cost, or else be driven from the market. It is a profit-and-loss system. Naturally, existing businesses generally prefer to keep out competitors in other ways. That is why the business community, despite its rhetoric, has so often been a major enemy of truly free enterprise.”

The danger of Kansas government having a friendly relationship with Kansas business is that the state will circumvent free markets and promote crony, or false, capitalism in Kansas. It’s something that we need to be on the watch for. The existence of the STAR bonds program lets us know that a majority of Kansas legislators — including many purported fiscal conservatives — prefer crony capitalism over free enterprise and genuine capitalism.

The problem

Government bureaucrats and politicians promote programs like STAR bonds as targeted investment in our economic future. They believe that they have the ability to select which companies are worthy of public investment, and which are not. It’s a form of centralized planning by the state that shapes the future direction of the Kansas economy.

As Hayek pointed out, knowledge that is important in the economy is dispersed. Consumers understand their own wants and business managers understand their technological opportunities and constraints to a greater degree than they can articulate and to a far greater degree than experts can understand and absorb.

When knowledge is dispersed but power is concentrated, I call this the knowledge-power discrepancy. Such discrepancies can arise in large firms, where CEOs can fail to appreciate the significance of what is known by some of their subordinates. … With government experts, the knowledge-power discrepancy is particularly acute.

Despite this knowledge problem, Kansas legislators are willing to give power to bureaucrats in the Department of Commerce and politicians on city councils who feel they have the necessary knowledge to direct the investment of public funds. One thing is for sure: the state and its bureaucrats and politicians have the power to make these investments. They just don’t have — they can’t have — the knowledge as to whether these are wise.

What to do The STAR bonds program is an “active investor” approach to economic development. Its government spending on business leads to taxes that others have to pay. That has a harmful effect on other business, both existing and those that wish to form.

Professor Art Hall of the Center for Applied Economics at the Kansas University School of Business is critical of this approach to economic development. In his paper Embracing Dynamism: The Next Phase in Kansas Economic Development Policy, Hall quotes Alan Peters and Peter Fisher: “The most fundamental problem is that many public officials appear to believe that they can influence the course of their state and local economies through incentives and subsidies to a degree far beyond anything supported by even the most optimistic evidence. We need to begin by lowering expectations about their ability to micro-manage economic growth and making the case for a more sensible view of the role of government — providing foundations for growth through sound fiscal practices, quality public infrastructure, and good education systems — and then letting the economy take care of itself.”

In the same paper, Hall writes this regarding “benchmarking” — the bidding wars for large employers that Kansas and many of its cities employ: “Kansas can break out of the benchmarking race by developing a strategy built on embracing dynamism. Such a strategy, far from losing opportunity, can distinguish itself by building unique capabilities that create a different mix of value that can enhance the probability of long-term economic success through enhanced opportunity. Embracing dynamism can change how Kansas plays the game.”

In making his argument, Hall cites research on the futility of chasing large employers as an economic development strategy: “Large-employer businesses have no measurable net economic effect on local economies when properly measured. To quote from the most comprehensive study: ‘The primary finding is that the location of a large firm has no measurable net economic effect on local economies when the entire dynamic of location effects is taken into account. Thus, the siting of large firms that are the target of aggressive recruitment efforts fails to create positive private sector gains and likely does not generate significant public revenue gains either.’”

There is also substantial research that is it young firms — distinguished from small business in general — that are the engine of economic growth for the future. We can’t detect which of the young firms will blossom into major success — or even small-scale successes. The only way to nurture them is through economic policies that all companies can benefit from. Reducing tax rates is an example of such a policy. Government spending on specific companies through programs like STAR bonds is an example of precisely the wrong policy.

We need to move away from economic development based on this active investor approach. We need to advocate for policies at all levels of government that lead to sustainable economic development. We need political leaders who have the wisdom to realize this, and the courage to act appropriately. Which is to say, to not act in most circumstances.

Industrial Revenue Bonds are a mechanism that Kansas cities and counties use to allow companies to avoid paying property and sales taxes.

Industrial Revenue Bonds are a confusing economic development program. We see evidence that citizens are concerned that the city or county is in the business of lending money to companies, when that is not the case. You see this misunderstanding revealed in comments left to newspaper articles reporting the issuance of IRBs, where comment writers complain that the city shouldn’t be in the business of lending companies money.

IRBs are not a loan by government

A recent Wichita city council agenda packet regarding an IRB issue explains that the city is not lending the applicant money. In fact, no one is lending, in the net: “Spirit AeroSystems, Inc. intends to purchase the bonds itself, through direct placement, and the bonds will not be reoffered for sale to the public.” If a company wants to lend itself money, this is a private transaction that should be of no public interest or concern.

Industrial Revenue Bonds in Kansas. Click for larger version.In 2010 when movie theater owner Bill Warren and partners sought IRBs, city documents held this: “American Luxury Cinemas, Inc. proposes to privately place the $16,000,000 taxable industrial revenue bond with Intrust Bank, with whom there is a long-standing banking relationship.” Again, if a bank wants to lend someone money, this a private transaction that should be of no public interest or concern.

The reason for IRBs

The reason why IRB transactions take place is simple: tax avoidance. That’s the real story of Industrial Revenue Bonds: Companies escape paying the property and sales taxes that you and I — as well as most business firms — must pay.

It’s not uncommon for the issuing company to buy the bonds, as in the case of Spirit. So why issue the bonds? The agenda packet has the answer: “The bond financed property will be eligible for sales tax exemption and property tax exemption for a term of ten years, subject to fulfillment of the conditions of the City’s public incentives policy.”

City documents didn’t give the amount of tax Spirit will avoid paying, so we’re left to surmise. Bonds could be issued up to $59.5 million. Taxable business property of that value would generate an annual tax bill of around $1.8 million per year, and Spirit would not pay that for up to ten years. For sales taxes, if all the purchased property was subject to sales tax, that one-time tax exemption would be $4.3 million. These are the upper bounds of the tax savings Spirit Aerosystems may receive. Its actual savings will probably be lower, but still substantial.

In the case of the Warren theater, the IRBs provided sales and property tax exemptions, although the property tax exemption was partially offset by a payment in lieu of taxes agreement.

IRBs are a confusing economic development program. It sounds like a loan from the city or state, but it’s not. The purpose is to convey tax avoidance.

Here’s language from the Wichita ordinance that was passed to implement the Spirit bonds: “The Bonds, together with the interest thereon, are not general obligations of the City, but are special obligations payable (except to the extent paid out of moneys attributable to the proceeds derived from the sale of the Bonds or to the income from the temporary investment thereof) solely from the lease payments under the Lease, and the Bond Fund and other moneys held by the Trustee, as provided in the Indenture. Neither the credit nor the taxing power of the State of Kansas or of any political subdivision of such State is pledged to the payment of the principal of the Bonds and premium, if any, and interest thereon or other costs incident thereto.”

So no governmental body has any obligation to pay the bondholders in case of default. But this language hints at another complicating factor of IRBs: The city actually owns the property purchased with the bond proceeds, and leases it to Spirit. Here’s the preamble of the ordinance: “An ordinance approving and authorizing the execution of a lease agreement between Spirit Aerosystems, Inc. and the City of Wichita, Kansas.”

Other language in the ordinance is “WHEREAS, the Company will acquire a leasehold interest in the Project from the City pursuant to said Lease Agreement.” There’s other language detailing the lease.

We create this “imaginary” lease agreement — and that’s what it is, as it doesn’t have the same purpose and economic meaning as most leases — for what purpose? Just so that certain companies can avoid paying taxes.

The City of Wichita does have another program that allows it to exempt these taxes under some circumstances without having to issue bonds. In this case the goal of the program is laid clear: tax avoidance.

The actual economic transaction

IRBs are a confusing program that obfuscates the actual economic transaction. That’s not good public policy, whether or not you agree with the concept of selective tax abatements as economic development.

Similarly, a principle of good tax policy is that those in similar situations should face the same laws. IRBs are contrary to this.

Also, IRBs are generally available only to large companies. There is massive red tape to overcome, as well as fees, such as an annual fee of $2,500 to the city.

Often when IRBs are presented to city councils for approval, there is explanation of what the bond proceeds will be used for. This is curious. It is as though city council members are wise enough to ascertain whether the plans a company has are economically feasible and desirable, and that the council would not grant approval for the IRBS if not.

While we can understand that citizens — with their busy lives — may not be informed or concerned about the complex workings of IRBs, we should expect more from our elected (and paid) officials. But we find often they are not informed.

As an example, in 2004 the Wichita Eagle reported: “In July, the council approved industrial revenue bond financing and a $1.7 million property tax abatement for Genesis Health Clubs. Council members later said they didn’t realize they had also approved a sales-tax break.” (Kolb goal : Full facts in future city deals, September 26, 2004)

Here we see Wichita City Council members not aware of the basic mechanism of a major city program that is frequently used. This is in spite of an informative city web page devoted to IRBs which prominently states: “Generally, property and services acquired with the proceeds of IRBs are eligible for sales tax exemption.”

In Kansas Community Improvement Districts, merchants charge additional sales tax for the benefit of the property owners, instead of the general public.

Community Improvement Districts are a relatively recent creation of the Kansas Legislature. In a CID, merchants charge additional sales tax, up to an extra two cents per dollar.

Community improvement district using bonds. Click for larger version.There are two forms of CID. Both start with the drawing of the boundaries of a geographical district. In the original form, a city borrows money by selling bonds. Then, the bond proceeds are given to the owners of the district. The bonds are repaid by the extra sales tax collected, known as the CID tax. The repayment period could be up to 22 years.

In the second form of CID, the extra sales tax is simply given to the owners of property in district as it is collected, after deduction of a small amount to reimburse government for its expenses. This is known as a “pay-as-you-go” CID.

The “pay-as-you-go” CID holds less risk for cities, as the extra sales tax — the CID tax — is remitted to the property owner as it is collected. If sales run below projections, or of the project never materializes, the property owners receive less funds, or no funds. With CID bonds, the city must pay back the bonds even if the CID tax does not raise enough funds to make the bond payments.

Community improvement district using pay-as-you-go. Click for larger version.Of note is that CID proceeds benefit the owners of the property, not the merchants. Kansas law requires that 55 percent of the property owners in the proposed CID agree to its formation. The City of Wichita uses a more restrictive policy, requiring all owners to consent.

Issues regarding CID

Perhaps the most important public policy issue regarding CIDs is this: If merchants feel they need to collect additional revenue from their customers, why don’t they simply raise their prices? But the premise of this question is not accurate, as it is not the merchants who receive CID funds. The more accurate question is why don’t landlords raise their rents? That puts them at a competitive disadvantage with property owners that are not within CIDs. Better for us, they rationalize, that unwitting customers pay higher sales taxes for our benefit.

Consumer protection Customers of merchants in CIDS ought to know in advance that an extra CID tax is charged. Some have recommended warning signage that protects customers from unknowingly shopping in stores, restaurants, and hotels that will be adding extra sales tax to purchases. Developers who want to benefit from CID money say that merchants object to signage, fearing it will drive away customers.

State law is silent on this. The City of Wichita requires a sign indicating that CID financing made the project possible, with no hint that customers will pay additional tax. The city also maintains a website showing CIDs. This form of notification is so weak as to be meaningless.

Eligible costs

One of the follies in government economic development policy is the categorization of costs into eligible and non-eligible costs. The proceeds from programs like CIDs and tax increment financing may be used only for costs in the “eligible” category. I suggest that we stop arbitrarily distinguishing between “eligible costs” and other costs. When city bureaucrats and politicians use a term like “eligible costs” it makes this process seem benign. It makes it seem as though we’re not really supplying corporate welfare and subsidy.

As long as the developer has to spend money on what we call “eligible costs,” the fact that the city subsidy is restricted to these costs has no economic meaning. Suppose I gave you $10 with the stipulation that you could spend it only on next Monday. Would you deny that I had enriched you by $10? Of course not. As long as you were planning to spend $10 next Monday, or could shift your spending from some other day to Monday, this restriction has no economic meaning.

Notification and withdrawal

If a merchant moves into an existing CID, how might they know beforehand that they will have to charge the extra sales tax? It’s a simple matter to learn the property taxes a piece of property must pay. But if a retail store moves into a vacant storefront in a CID, how would this store know that it will have to charge the extra CID sales tax? This is an important matter, as the extra tax could place the store at a competitive disadvantage, and the prospective retailer needs to know of the district’s existence and its terms.

Then, if a business tires of being in a CID — perhaps because it realizes it has put itself at a competitive disadvantage — how can the district be dissolved?

The nature of taxation

CIDs allow property owners to establish their own private taxing district for their exclusive benefit. This goes against the grain of the way taxes are usually thought of. Generally, we use taxation as a way to pay for services that everyone benefits from, and from which we can’t exclude people. An example would be police protection. Everyone benefits from being safe, and we can’t exclude people from participating in — benefiting from — police protection.

But CIDs allow taxes to be collected for the benefit of one specific entity. This goes against the principle of broad-based taxation to pay for an array of services for everyone. But in this case, the people who benefit from the CID are quite easy to identify: the property owners in the district.