Tag: Economic development

-

Another week in Wichita, more CID sprawl

Shoppers in west Wichita should prepare to pay higher taxes, if the city approves a Community Improvement District at Kellogg and West Streets.

-

Wichita CID illustrates pitfalls of government intervention

A proposed special tax district in Wichita holds the potential to harm consumers, the city’s reputation, and the business prospects of competitors. Besides, we shouldn’t let private parties use a government function for their exclusive benefit.

-

Wichita Business Journal reporting misses the point

Reporting by the Wichita Business Journal regarding economic development incentives in Wichita makes a big mistake in overlooking where the real money is.

-

Wichita property tax delinquency problem not solved

Despite a government tax giveaway program, problems with delinquent special assessment taxes in Wichita have become worse.

-

Wichita’s WaterWalk apartment deal

Wichita is ready to consider another giveaway to politically-connected interests at the expense of citizens and taxpayers.

-

Wichita Chamber speaks on county spending and taxes

The Wichita Metro Chamber of Commerce urges spending over fiscally sound policies and tax restraint in Sedgwick County.

-

Cost of restoring quality of life spending cuts in Sedgwick County: 43 deaths

An analysis of public health spending in Sedgwick County illuminates the consequences of public spending decisions. In particular, those calling for more spending on zoos and arts must consider the lives that could be saved by diverting this spending to public health, according to analysis from Kansas Health Institute.

-

In Wichita, an incomplete economic development analysis

The Wichita City Council will consider an economic development incentive based on an analysis that is nowhere near complete.

-

In Sedgwick County, expectation of government entitlements

In Sedgwick County, we see that once companies are accustomed to government entitlements, any reduction is met with resistance.

-

Cash incentives in Wichita

Wichita city leaders are proud to announce the end of cash incentives, but they were only a small portion of the total cost of incentives.

-

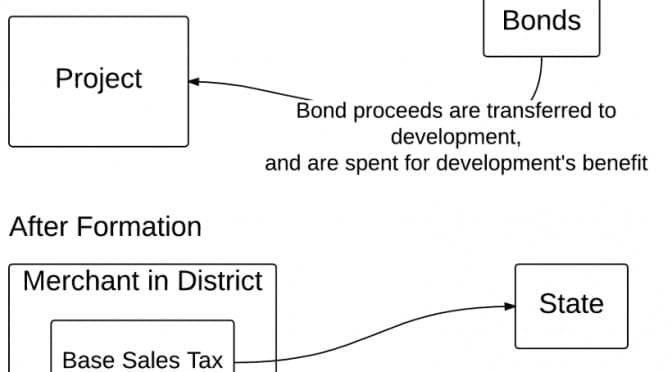

In Wichita, benefitting from your sales taxes, but not paying their own

A Wichita real estate development benefits from the sales taxes you pay, but doesn’t want to pay themselves.

-

For Sedgwick County Zoo, a moratorium on its commitment

As the Sedgwick County Zoo and its supporters criticize commissioners for failing to honor commitments, the Zoo is enjoying a deferral of loan payments and a break from accumulating interest charges.