Tag: Wichita city government

-

WichitaLiberty.TV: Kansas Policy Institute Vice President and Policy Director James Franko

Kansas Policy Institute has produced a study of the effect of state and local regulation on business. James Franko of KPI discusses.

-

Wichita city council member Jeff Longwell should not have voted

A sequence of events involving Jeff Longwell should concern citizens as they select the next Wichita mayor. Based on Wichita law, Longwell should not have voted on a matter involving the Ambassador Hotel, either for or against it.

-

Study on state and local regulation released

This week Kansas Policy Institute released a study of regulation and its impact at the state and local level. This is different from most investigations of regulation, as most focus on federal regulations.

-

Ranzau, Peterjohn endorse Sam Williams for Wichita mayor

Despite their differences, two members of the Sedgwick County Commission have endorsed Sam Williams for Wichita Mayor.

-

Downtown Wichita deal shows some of the problems with the Wichita economy

In this script from a recent episode of WichitaLiberty.TV: A look at the Wichita city council’s action regarding a downtown Wichita development project and how it is harmful to Wichita taxpayers and the economy.

-

Voter turnout, Wichita primary election, March 3, 2015

The Sedgwick County Election Office reports that for the March 3, 2015 primary election there were 200,371 registered voters in the City of Wichita. 19,605 ballots were cast, for a turnout rate of 9.8 percent. View a map of turnout by precinct below, or click here to open in a new window.

-

Wichita mayoral candidates at Pachyderm Club

Wichita mayoral candidates Jeff Longwell and Sam Williams at the Wichita Pachyderm Club.

-

A Wichita Shocker, redux

Based on events in Wichita, the Wall Street Journal wrote “What Americans seem to want most from government these days is equal treatment. They increasingly realize that powerful government nearly always helps the powerful …” But Wichita’s elites don’t seem to understand this.

-

WichitaLiberty.TV: A downtown Wichita deal shows some of the problems with the Wichita economy

In this episode of WichitaLiberty.TV: We’ll examine the city council’s action regarding a downtown Wichita development project and how it is harmful to Wichita taxpayers and the economy.

-

How TIF routes taxpayer-funded benefits to Wichita’s political players

In Wichita, tax increment financing (TIF) leads to taxpayer-funded waste that benefits those with political connections at city hall.

-

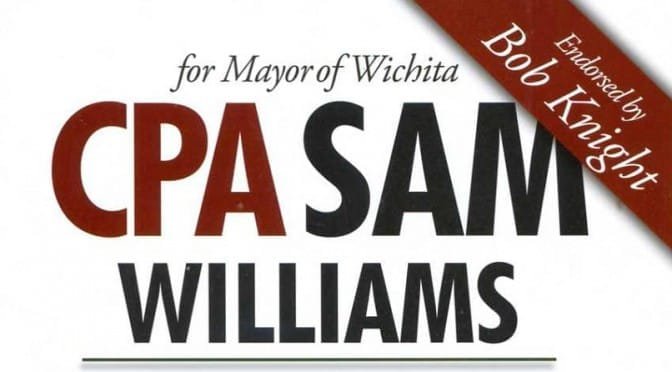

Sam Williams, CPA?

Sam Williams, a candidate for Wichita mayor, is not entitled to use the title “CPA,” according to Kansas law.

-

Wichita officials complain of lack of cash for incentives

Wichita has stepped up with cash for incentives when needed, contrary to complaints of economic development officials.