Tag: Cronyism

-

Historic preservation tax credits, or developer welfare?

A Wichita developer seeks to have taxpayers fund a large portion of his development costs, using a wasteful government program of dubious value.

-

Campaign contribution changes in Wichita

A change to Wichita city election law is likely to have little practical effect.

-

Wichita officials, newspaper, just don’t get it on Ex-Im Bank

Wichita’s establishment prefers cronyism over capitalism.

-

Bombardier can be a learning experience

The unfortunate news of the cancellation of a new aircraft program can be a learning opportunity for Wichita.

-

Wichita Chamber calls for more cronyism

By advocating for revival of the Export-Import Bank of the United States, the Wichita Metro Chamber of Commerce continues its advocacy for more business welfare, more taxes, more wasteful government spending, and more cronyism

-

Export-Import Bank threatens a revival

Business groups and government agencies usually favor Ex-Im. Free-market and capitalism advocacy groups are almost universally opposed.

-

Another week in Wichita, more CID sprawl

Shoppers in west Wichita should prepare to pay higher taxes, if the city approves a Community Improvement District at Kellogg and West Streets.

-

Wichita CID illustrates pitfalls of government intervention

A proposed special tax district in Wichita holds the potential to harm consumers, the city’s reputation, and the business prospects of competitors. Besides, we shouldn’t let private parties use a government function for their exclusive benefit.

-

Wichita property tax delinquency problem not solved

Despite a government tax giveaway program, problems with delinquent special assessment taxes in Wichita have become worse.

-

In Sedgwick County, expectation of government entitlements

In Sedgwick County, we see that once companies are accustomed to government entitlements, any reduction is met with resistance.

-

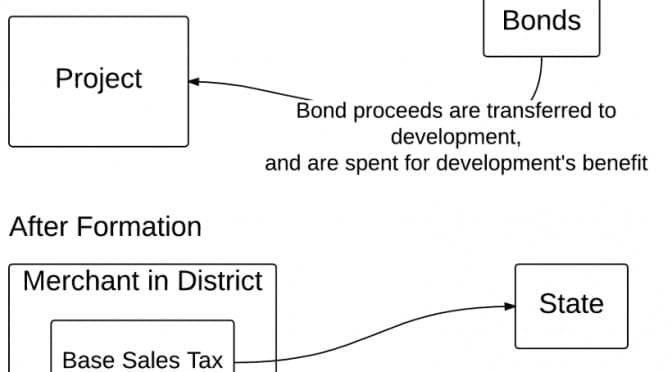

In Wichita, benefitting from your sales taxes, but not paying their own

A Wichita real estate development benefits from the sales taxes you pay, but doesn’t want to pay themselves.

-

Kansas senators vote to advance Ex-Im Bank

Kansas senators vote to advance Ex-Im Bank