The Wichita Eagle shows how its adherence to ideology misinforms Kansans and limits their exposure to practical solutions for governance.

In an op-ed posted the day before election day, the editorial board of the Wichita Eagle wrote of the problems it believes the next Kansas governor will face:

The candidates vying to be Kansas governor have lofty-sounding goals and campaign promises. But here’s the grim reality: Whoever wins Tuesday will spend the next several years trying to fill a budget hole.

And that hole keeps growing deeper. (“Budget hole awaits winner,” November 3, 2014)

The state has to make changes. We’ve cut taxes, but we’ve not yet met the challenge of cutting spending to match. The problem with this op-ed is the assertion that will take several years to fix. Here’s what I left in reply:

I have to disagree. Kansas Policy Institute has examined the Kansas budget and found ways to make several structural changes that would immediately (within one year) balance the Kansas budget. This would preserve existing services and fully fund the increases in K-12 school spending and social service caseloads that Kansas Legislative Research has projected. The policy brief that KPI has prepared on this matter is only ten pages long and not difficult to comprehend.

The changes that KPI recommends are specific adjustments to the way Kansas spends money. They are not the vague calls to eliminate waste that we see politicians campaign on. This is something that Kansas could do if both Democrats and Republicans have the will.

Dave Trabert, president of Kansas Policy Institute, added this:

Bob is right. And the Eagle is well aware of our budget plan but declines to let readers know that the budget can be balanced without service reductions or tax increases. It won’t take “several years” to fix the budget; our plan could be implemented by passing a few pieces of legislation.

Campaign methods used in the recent election may spark debate on the information government makes available about voters and their voting behavior.

This election day, after voting, someone posted on their Facebook page: “I’m not comfortable with the GOP observer writing down the names of those who appear to vote.”

Elsewhere on Facebook and other online sites stories like this were common: “I received a palm card that had names and addresses of my neighbors, and whether they voted in the last four elections. This was supposed to motivate me, a woman voter, to vote. It actually freaked me out that someone is distributing that information without my consent.”

The practice referred to in the first comment — poll watching — is common and has been used for decades. The practice objected to by the second writer is new. By sending mail or email informing people of the voting practices of their neighbors, campaigns attempt to shame people into voting. Research suggests shaming is effective in motivating people to vote.

Both major parties and independent groups from all sides of the political spectrum used this technique this year.

From social media and news stories, it seems that people are surprised to learn that their voter information is a public record. It’s important to know that the contents of your ballot — that is, which candidates you voted for — is secret. Here’s what anyone can acquire in Kansas about voters (other states may be different, but I think most are similar):

Voter registration ID number, name, address, mailing address, gender, date of registration, date of birth, telephone number (if the voter supplies it; it is not required) whether the voter is on the permanent advance list, party registration, precinct number, and all the different jurisdictions the voter lives in such as city council district, county commission district, school district, Kansas House and Senate districts, and others.

Then, for each election you can learn whether the voter voted, and by which method (mail, advance in person, polling place). For primary elections, you can learn whether the voter selected a Republican or Democratic ballot.

(I should mention that in Kansas this information is supplied in a clumsy format that is difficult to use. I’ve developed procedures whereby I restructure this data to a relational data model that allows for proper analysis.)

Other organizations may enhance these records with data of their own. For example, in the government-supplied voter file, many telephone numbers are missing. Others are out-of-date, especially as households abandon traditional telephone service for cell phones. So candidates may use services that provide telephone numbers given names and addresses. Or, organizations may add other data purchased from marketing research services, such as magazines subscribed to, etc.

It would be useful to have a debate over whether the fact of being a registered voter and the act of voting should be a public record. This is the first election where people have become widely aware of the nature of the voting information that is available, and how campaigns and advocacy groups use it. I wonder if the new awareness of the availability of this information will deter people from registering and voting?

As far as government transparency and open records is concerned, we can distinguish voting data from other government data. When we ask for records of spending, contracts, correspondence, and the like, we asking for information about government and the actions government has taken.

But voter data is information about action taken by people, not by government. There’s a difference.

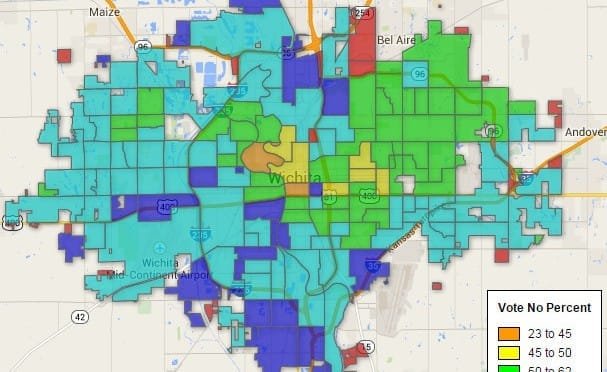

Here’s a map I created of the “No” vote percentage by precinct. To use an interactive version of this map, click here. On the interactive map you may scroll and zoom, and you may click on a precinct for more information.

Citizens want to trust their hometown newspaper as a reliable source of information. The Wichita Eagle has not only fallen short of this goal, it seems to have abandoned it.

The Wichita Eagle last week published a fact-check article titled “Fact check: ‘No’ campaign ad on sales tax misleading.” As of today, the day before the election, I’ve not seen any similar article examining ads from the “Yes Wichita” group that campaigns for the sales tax. Also, there has been little or no material that examined the city’s claims and informational material in a critical manner.

Wichita Eagle Building, detailSomeone told me that I should be disappointed that such articles have not appeared. I suppose I am, a little. But that is balanced by the increasing awareness of Wichitans that the Wichita Eagle is simply not doing its job.

It’s one thing for the opinion page to be stocked solely with liberal columnists and cartoonists, considering the content that is locally produced. But newspapers like the Eagle tell us that the newsroom is separate from the opinion page. The opinion page has endorsed passage of the sales tax. As far as the newsroom goes, by printing an article fact-checking one side of an issue and failing to produce similar pieces for the other side — well, readers are free to draw their own conclusions about the reliability of the Wichita Eagle newsroom.

As a privately-owned publication, the Wichita Eagle is free to do whatever it wants. But when readers see obvious neglect of a newspaper’s duty to inform readers, readers are correct to be concerned about the credibility of our state’s largest newspaper.

Citizens want to trust their hometown newspaper as a reliable source of information. The Wichita Eagle has not only fallen short of this goal, it seems to have abandoned it.

Here are some topics and questions the Eagle could have examined in fact-checking articles on the “Yes Wichita” campaign and the City of Wichita’s informational and educational campaign.

The Wichita Eagle could start with itself and explain why it chose a photograph of an arterial street to illustrate a story on a sales tax that is dedicated solely for neighborhood streets. The caption under the photo read “Road construction, such as on East 13th Street between Oliver and I-135, would be part of the projects paid for by a city sales tax.”

Issues regarding “Yes Wichita”

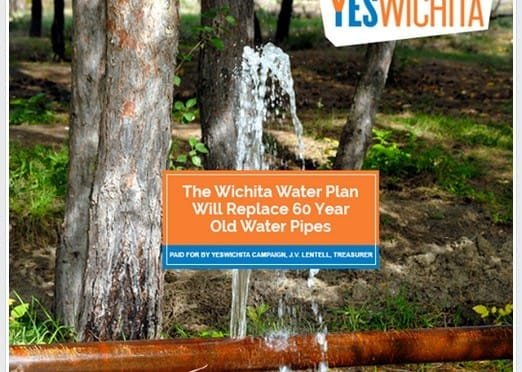

The “Yes Wichita” campaign uses an image of bursting wooden water pipes to persuade voters. Does Wichita have any wooden water pipes? And isn’t the purpose of the sales tax to build one parallel pipeline, not replace old water pipes? See Fact-checking Yes Wichita: Water pipe(s).

The “Yes Wichita” campaign group claims that the sales tax will replace old rusty pipes that are dangerous. Is that true?

The City and “Yes Wichita” give voters two choices regarding a future water supply: Either vote for the sales tax, or the city will use debt to pay for ASR expansion and it will cost an additional $221 million. But the decision to use debt has not been made, has it? Wouldn’t the city council have to vote to issue those bonds? Is there any guarantee that the council will do that?

The “Yes Wichita” group says that one-third of the sales tax will be paid by visitors to Wichita. But the city’s documents cite the Kansas Department of Revenue which gives the number as 13.5 percent. Which is correct? This is a difference of 2.5 times in the estimate of Wichita sales tax paid by visitors. This is a material difference in something used to persuade voters.

The city’s informational material states “The City has not increased the mill levy rate for 21 years.” In 1994 the Wichita mill levy rate was 31.290, and in 2013 it was 32.509. That’s an increase of 1.219 mills, or 3.9 percent. The Wichita City Council did not take explicit action, such as passing an ordinance, to raise this rate. Instead, the rate is set by the county based on the city’s budgeted spending and the assessed value of taxable property subject to taxation by the city. While the city doesn’t have control over the assessed value of property, it does have control over the amount it decides to spend. Whatever the cause, the mill levy has risen. See Fact-checking Yes Wichita: Tax rates.

“Yes Wichita” says there is a plan for the economic development portion of the sales tax. If the plan for economic development is definite, why did the city decide to participate in the development of another economic development plan just last month? What if that plan recommends something different than what the city has been telling voters? And if the plan is unlikely to recommend anything different, why do we need it?

Citizens have asked to know more about the types of spending records the city will provide. Will the city commit to providing checkbook register-level spending data? Or will the city set up separate agencies to hide the spending of taxpayer funds like it has with the Wichita Downtown Development Corporation, Go Wichita Convention and Visitors Bureau, and Greater Wichita Economic Development Corporation?

Issues regarding the City of Wichita

Mayor Carl Brewer said the city spent $47,000 of taxpayer funds to send a letter and brochure to voters because he was concerned about misinformation. In light of some of the claims made by the “Yes Wichita” group, does the city have plans to inform voters of that misinformation?

Hasn’t the city really been campaigning in favor of the sales tax? Has the city manager been speaking to groups to give them reasons to vote against the tax? Does the city’s website provide any information that would give voters any reason to consider voting other than yes?

The “Yes Wichita” group refers voters to the city’s website and information to learn about the sales tax issue. Since the “Yes Wichita” group campaigns for the sales tax, it doesn’t seem likely it would refer voters to information that would be negative, or even neutral, towards the tax. Is this evidence that the city is, in fact, campaigning for the sales tax?

The “Yes Wichita” group says that one-third of the sales tax will be paid by visitors to Wichita. But the city’s documents cite the Kansas Department of Revenue which gives the number as 13.5%. Which is correct? This is a difference of 2.5 times in the estimate of Wichita sales tax paid by visitors. This is a material difference in something used to persuade voters. If “Yes Wichita” is wrong, will the city send a mailer to correct the misinformation?

The city’s informational material states “The City has not increased the mill levy rate for 21 years.” But the city’s comprehensive annual financial reports show that in 1994 the Wichita mill levy rate was 31.290, and in 2013 it was 32.509. That’s an increase of 1.219 mills, or 3.9 percent. The Wichita City Council did not take explicit action, such as passing an ordinance, to raise this rate. Instead, the rate is set by the county based on the city’s budgeted spending and the assessed value of taxable property subject to taxation by the city. While the city doesn’t have control over the assessed value of property, it does have control over the amount it decides to spend. Whatever the cause, the mill levy has risen. Is this misinformation that needs to be corrected?

The city says that the ASR project is a proven solution that will provide for Wichita’s water needs for a long time. Has the city told voters that the present ASR system had its expected production rate cut in half? Has the city presented to voters that the present ASR system is still in its commissioning phase, and that new things are still being learned about how the system operates?

The City and “Yes Wichita” give voters two choices regarding a future water supply: Either vote for the sales tax, or the city will use debt to pay for ASR expansion and it will cost an additional $221 million. But the decision to use debt has not been made, has it? Wouldn’t the city council have to vote to issue those bonds? Is the any guarantee that the council will do that?

If the plan for economic development is definite, why did the city decide to participate in the development of another economic development plan just last month? What if that plan recommends something different than what the city has been telling voters? And if the plan is unlikely to recommend anything different, why do we need it?

Citizens have asked to know more about the types of spending records the city will provide. Will the city commit to providing checkbook register-level spending data? Or will the city set up separate agencies to hide the spending of taxpayer funds like it has with the Wichita Downtown Development Corporation, Go Wichita Convention and Visitors Bureau, and Greater Wichita Economic Development Corporation?

The “Yes Wichita” campaign uses an image of bursting wooden water pipes to persuade voters. Does Wichita have any wooden water pipes? And isn’t the purpose of the sales tax to build one parallel pipeline, not replace old water pipes? If this advertisement by “Yes Wichita” is misleading, will the city send an educational mailing to correct this?

The Yes Wichita campaign group claims that the sales tax will replace old rusty pipes that are dangerous. Is that true? If not, will the city do anything to correct this misinformation?

Campaign activity by the Wichita Downtown Development Corporation appears to be contrary to several opinions issued by Kansas Attorneys General regarding the use of public funds in elections.

While the Wichita Downtown Development Corporation presents itself as a non-profit organization that is independent of the City of Wichita, it receives 95 percent of its revenue from taxes, according to its most recent IRS Form 990. While Kansas has no statutes or court cases prohibiting the use of public funds for electioneering, there are at least two Kansas Attorney General opinions on this topic.

One, opinion 93-125, states in its synopsis: “The public purpose doctrine does not encompass the use of public funds to promote or advocate a governing body’s position on a matter which is before the electorate. However, public funds may be expended to educate and inform regarding issues to be voted upon by the electorate.”

Campaign activity at the office of the Wichita Downtown Development Corporation.The “governing body” in this instance is the Wichita City Council.

While some governing bodies spend taxpayer funds to present information about ballot measures, this is not the case with the Wichita Downtown Development Corporation. It explicitly campaigns in favor of the issue. It displays pro-sales tax campaign signs at its office. It publicly endorsed passage of the sales tax.

A more recent Kansas Attorney General opinion, 2001-13, holds this language: “While the Kansas appellate courts have not directly addressed the issue of whether public funds can be used to promote a position during an election, there are a number of cases from other jurisdictions that conclude that a public entity cannot do so.”

The opinion cites a court case: “Underlying this uniform judicial reluctance to sanction the use of public funds for election campaigns rests an implicit recognition that such expenditures raise potentially serious constitutional questions. A fundamental precept of this nation’s democratic electoral process is that the government may not ‘take sides’ in election contests or bestow an unfair advantage on one of several competing factions.”

The opinion reaffirms 93-125, stating: “In Attorney General Opinion No. 93-125, Attorney General Robert T. Stephan concluded that public funds may not be used to promote or advocate a city governing body’s position on a matter that is before the electorate.”

Given these Kansas Attorney General opinions, and considering good public policy, Wichita voters need to ask: Should an organization that is funded 95 percent by taxes be campaigning for a ballot issue?

The “Yes Wichita” campaign group makes a Facebook post with false information to Wichita voters. Will Wichita Mayor Carl Brewer send a mailer to Wichitans warning them of this misleading information?

“Yes Wichita” Facebook post. Click for larger version.Here’s a post from the “Yes Wichita” Facebook page. This group campaigns in favor of the one cent per dollar Wichita sales tax that is on the November ballot.

The claim made in this post is incorrect and misleading.

The sales tax plan regarding water calls for the augmentation of one pipe, as shown in this table from the city’s plan. The plan does not say, or imply, replacing pipes, as this advertisement indicates.

The plan also says that sales tax revenue “Builds an additional pipeline.” Not “Replace 60 year old water pipes” as promoted to voters by “Yes Wichita.” The plan builds an additional parallel pipeline.

Wichita Water Supply Plan Capital CostsPlus, the pipe that is the subject of the city’s water plan is 60 years old, but there is no indication that it needs replacement.

A Wichita company asks for property and sales tax exemptions on the same day Wichita voters decide whether to increase the sales tax, including the tax on groceries.

This week the Wichita City Council will hold a public hearing concerning the issuance of Industrial Revenue Bonds to Spirit AeroSystems, Inc. The purpose of the bonds is to allow Spirit to avoid paying property taxes on taxable property purchased with bond proceeds for a period of five years. The abatement may then be extended for another five years. Additionally, Spirit will not pay sales taxes on the purchased property.

City documents state that the property tax abatement will be shared among the taxing jurisdictions in these estimated amounts:

No value is supplied for the amount of sales tax that may be avoided. The listing of USD 259, the Wichita public school district, is likely an oversight by the city, as the Spirit properties lie in the Derby school district. This is evident when the benefit-cost ratios are listed:

City of Wichita: 1.98 to one

General Fund: 1.78 to one

Debt Service: 2.34 to one

Sedgwick County: 1.54 to one

U.S.D. 260: 1.00 to one (Derby school district)

State of Kansas: 28.23 to one

The City of Wichita has a policy where economic development incentives should have a benefit cost ratio of 1.3 to one or greater for the city to participate, although there are many loopholes the city regularly uses to approve projects with smaller ratios. Note that the ratio for the Derby school district is 1.00 to one, far below what the city requires for projects it considers for participation. That is, unless it uses one of the many available loopholes.

We have to wonder why the City of Wichita imposes upon the Derby school district an economic development incentive that costs the Derby schools $143,038 per year, with no payoff? Generally the cost of economic development incentives are shouldered because there is the lure of a return, be it real or imaginary. But this is not the case for the Derby school district. This is especially relevant because the school district bears, by far, the largest share of the cost of the tax abatement.

Of note, the Derby school district extends into Wichita, including parts of city council districts 2 and 3. These districts are represented by Pete Meitzner and James Clendenin, respectively.

The city’s past experience

Spirit Aerosystems is a spin-off from Boeing and has benefited from many tax abatements over the years. In a written statement in January 2012 at the time of Boeing’s announcement that it was leaving Wichita, Mayor Carl Brewer wrote “Our disappointment in Boeing’s decision to abandon its 80-year relationship with Wichita and the State of Kansas will not diminish any time soon. The City of Wichita, Sedgwick County and the State of Kansas have invested far too many taxpayer dollars in the past development of the Boeing Company to take this announcement lightly.”

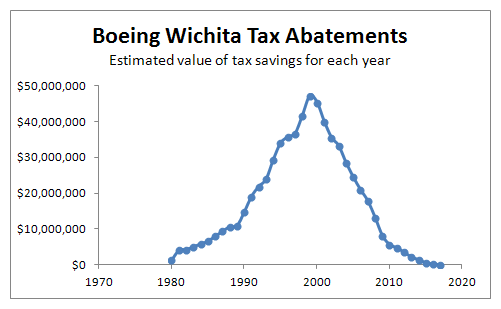

Along with the mayor’s statement the city released a compilation of the industrial revenue bonds authorized for Boeing starting in 1979. The purpose of the IRBs is to allow Boeing to escape paying property taxes, and in many cases, sales taxes. According to the city’s compilation, Boeing was granted property tax relief totaling $657,992,250 from 1980 to 2017. No estimate for the amount of sales tax exemption is available. I’ve prepared a chart showing the value of property tax abatements in favor of Boeing each year, based on city documents. There were several years where the value of forgiven tax was over $40 million.

Boeing Wichita tax abatements, annual value, from City of Wichita.Kansas Representative Jim Ward, who at the time was Chair of the South Central Kansas Legislative Delegation, issued this statement regarding Boeing and incentives:

Boeing is the poster child for corporate tax incentives. This company has benefited from property tax incentives, sales tax exemptions, infrastructure investments and other tax breaks at every level of government. These incentives were provided in an effort to retain and create thousands of Kansas jobs. We will be less trusting in the future of corporate promises.

Not all the Boeing incentives started with Wichita city government action. But the biggest benefit to Boeing, which is the property tax abatements through industrial revenue bonds, starts with Wichita city council action. By authorizing IRBs, the city council cancels property taxes not only for the city, but also for the county, state, and school district.

In this episode of WichitaLiberty.TV: Dave Trabert of Kansas Policy Institute talks about KPI’s recent policy brief “A Five-Year Budget Plan for the State of Kansas: How to balance the budget and have healthy ending balances without tax increases or service reductions.” View below, or click here to view at YouTube. Episode 64, broadcast November 2, 2014.

At a forum on October 28, “Yes Wichita” co-chair Moji Fanimokun told the audience that “Property taxes haven’t been raised in over 21 years in Wichita.”

This claim — that the mill levy has not been raised for a long time — is commonly made by the city and “Yes Wichita” supporters. It’s useful to take a look at actual numbers to see what has happened.

In 1994 the Wichita mill levy rate was 31.290, and in 2013 it was 32.509. That’s an increase of 1.219 mills, or 3.9 percent. The Wichita City Council did not take explicit action, such as passing an ordinance, to raise this rate. Instead, the rate is set by the county based on the city’s budgeted spending and the assessed value of taxable property subject to taxation by the city. While the city doesn’t have control over the assessed value of property, it does have control over the amount it decides to spend. Whatever the cause, the mill levy has risen, contrary to the claims of “Yes Wichita.”

Apart from the focus on the mill levy, voters may want to know that the dollars of property tax the city collects has risen. This growth comes from new property being created (although old property disappears, too), and from increases in assessed value of existing property. From 1994 to 2011 property tax revenue increased from $58.672 to $119.745 million, or 104 percent. We didn’t experience anything near that rate of growth in the combination of population or inflation. It’s true that these values have slowed in growth or even declined in recent years. But that’s a symptom of the problem: When tax revenue increases, so to does spending, and we become accustomed to a certain level. When revenue increases don’t keep pace with history, government finds it difficult to make the necessary cuts.

This claim — that the mill levy has not been raised for a long time — is commonly made by the city and “Yes Wichita” supporters. It’s useful to take a look at actual numbers to see what has happened.

This claim — that the mill levy has not been raised for a long time — is commonly made by the city and “Yes Wichita” supporters. It’s useful to take a look at actual numbers to see what has happened. Apart from the focus on the mill levy, voters may want to know that the dollars of property tax the city collects has risen. This growth comes from new property being created (although old property disappears, too), and from increases in assessed value of existing property. From 1994 to 2011 property tax revenue increased from $58.672 to $119.745 million, or 104 percent. We didn’t experience anything near that rate of growth in the combination of population or inflation. It’s true that these values have slowed in growth or even declined in recent years. But that’s a symptom of the problem: When tax revenue increases, so to does spending, and we become accustomed to a certain level. When revenue increases don’t keep pace with history, government finds it difficult to make the necessary cuts.

Apart from the focus on the mill levy, voters may want to know that the dollars of property tax the city collects has risen. This growth comes from new property being created (although old property disappears, too), and from increases in assessed value of existing property. From 1994 to 2011 property tax revenue increased from $58.672 to $119.745 million, or 104 percent. We didn’t experience anything near that rate of growth in the combination of population or inflation. It’s true that these values have slowed in growth or even declined in recent years. But that’s a symptom of the problem: When tax revenue increases, so to does spending, and we become accustomed to a certain level. When revenue increases don’t keep pace with history, government finds it difficult to make the necessary cuts.