Tag: Featured

-

Greater Wichita Partnership asks for help

Wichita’s economic development agency asks for assistance in developing its focus and strategies.

-

WichitaLiberty.TV: Danedri Herbert, Editor of The Sentinel

The Sentinel’s Danedri Herbert joins Bob Weeks to discuss the upcoming gubernatorial debate, the Kansas Legislature’s website and transparency, and accountability in government.

-

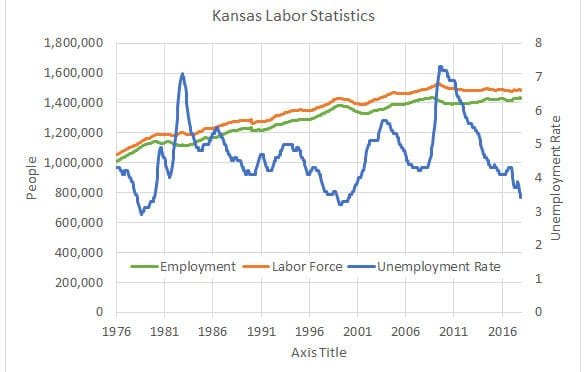

Unemployment in Kansas

New Kansas Governor Jeff Colyer proudly cites the low Kansas unemployment rate, but there is more to the story.

-

WichitaLiberty.TV: Sound money and private governance

Professor Edward Stringham joins Karl Peterjohn and Bob Weeks to discuss Bitcoin, sound money, and the role of markets in private governance.

-

WichitaLiberty.TV: WATC and WSU Tech President Sheree Utash

Wichita Area Technical College (WATC) has formed an affiliation with Wichita State University, to be called the Wichita State University Campus of Applied Sciences and Technology, or WSU Tech. Sheree Utash, president of WATC and future president of WSU Tech, joins Karl Peterjohn to discuss these institutions.

-

Dale Dennis, sage of Kansas school finance?

Is the state’s leading expert on school funding truly knowledgeable, or is he untrustworthy?

-

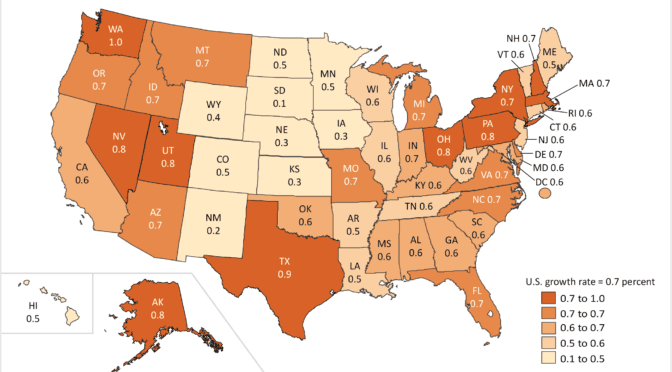

Kansas GDP growth

Kansas ranks low among the states in growth of gross domestic product (GDP) for the third quarter of 2017.

-

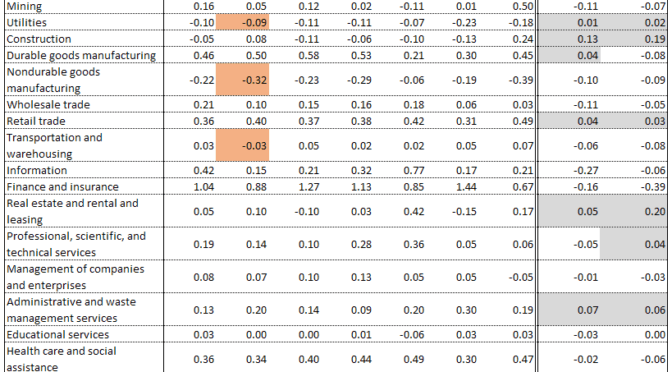

Personal income growth in Kansas

Personal income growth in Kansas trails most of the nation.

-

WichitaLiberty.TV: Radio Host Andy Hooser

Radio Host Andy Hooser of the Voice of Reason appears with Karl Peterjohn to discuss the simulcast of his radio show on KGPT 26, the legislative session, and whether President Trump’s tax breaks can save Kansas from the recent tax hike.

-

WichitaLiberty.TV: Kansas State of the State for 2018

James Franko of Kansas Policy Institute joins Karl Peterjohn to discuss Governor Brownback’s State of the State Address for 2018. Topics include schools and Medicaid expansion.

-

WichitaLiberty.TV: Looking back at 2017

Karl Peterjohn and Bob Weeks look back at some stories from 2017, and take a peek at the year ahead.

-

In Wichita, three Community Improvement Districts to be considered

In Community Improvement Districts (CID), merchants charge additional sales tax for the benefit of the property owners, instead of the general public. Wichita may have an additional three, contributing to the problem of CID sprawl.