Tag: Featured

-

A big-picture look at the EDA

While praising the U.S. Economic Development Administration for a small grant to a local institution, the Wichita Eagle editorial board overlooks the big picture.

-

WichitaLiberty.TV: Bad news from Topeka on taxes and schools, and also in Wichita. Also, a series of videos that reveal the nature of government.

In this episode of WichitaLiberty.TV: The sales tax increase is harmful and not necessary. Kansas school standards are again found to be weak. The ASR water project is not meeting expectations. Then, the Independent Institute has produced a series of videos that illustrate the nature of government. Episode 88, broadcast July 19, 2015.

-

Discussion of open government in Wichita and Kansas

Perspectives may differ, but the point is the same — more government transparency leads to more citizen engagement and better outcomes in communities, states, and nations.

-

‘Love Gov’ humorous and revealing of government’s nature

A series of short videos from the Independent Institute entertains and teaches lessons at the same time.

-

Kansas school standards evaluated

A new edition of an ongoing study shows that Kansas school standards are weak, compared to other states. This is a continuation of a trend.

-

In Wichita, wasting electricity a chronic problem

The chronic waste of electricity in downtown Wichita is a problem that probably won’t be solved soon, given the city’s attitude.

-

Wichita water statistics update

The Wichita ASR water project had a relatively good month in June, but has not been producing water at the projected rate or design capacity.

-

Wichita property taxes still high, but comparatively better

An ongoing study reveals that generally, property taxes on commercial and industrial property in Wichita are high. In particular, taxes on commercial property in Wichita are among the highest in the nation, although Wichita has improved comparatively.

-

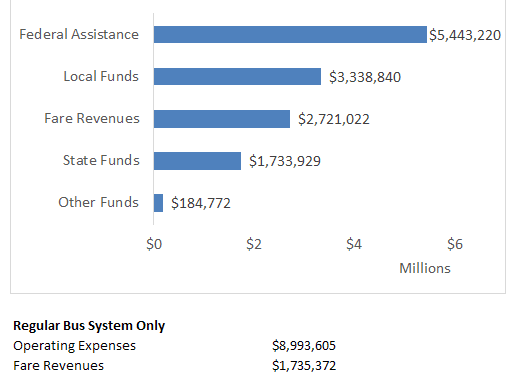

Wichita Transit snapshot

Wichita Transit snapshot

-

In Wichita, open records relief may be on the way

A new law in Kansas may provide opportunities for better enforcement of the Kansas Open Records Act.

-

Kansas sales tax has disproportionate harmful effects

Kansas legislative and executive leaders must realize that a shift to consumption taxes must be accompanied by relief from its disproportionate harm to low-income households.

-

How to turn $399,000 into $65,000 in downtown Wichita

Once embraced by Wichita officials as heroes, real estate listings for two floors of a downtown Wichita office building illustrate the carnage left behind by two developers