Tag: Kansas Governor

-

In Kansas, the war on property rights

John Todd makes an appearance on The Voice of Reason with Andy Hooser to talk about proposed legislation in Kansas that would be harmful to private property rights.

-

Lessons from Kansas tax reform

What can the rest of the nation learn from our experience in Kansas? Come to think of it, why haven’t we learned much?

-

WichitaLiberty.TV: Kansas Director of Budget Shawn Sullivan

Kansas Director of Budget Shawn Sullivan joins Karl Peterjohn and Bob Weeks to explain issues related to the Kansas budget.

-

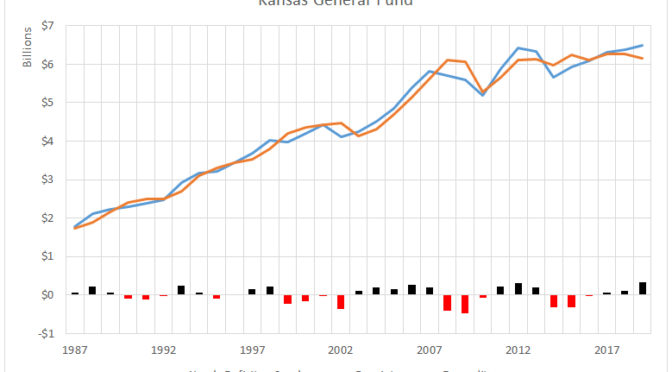

Kansas general fund

Data and charts regarding the Kansas general fund.

-

WichitaLiberty.TV: Kansas politics, school choice, and asset forfeiture

Co-host Karl Peterjohn joins Bob Weeks to discuss a few big developments in Kansas politics, school choice, and civil asset forfeiture.

-

Again, KPERS shows why public pension reform is essential

Proposals in the Kansas budget for fiscal year 2018 are more evidence of why defined-benefit pension plans are incompatible with the public sector.

-

Holding politicians to their boasts and promises

There are useful lessons we can learn from the criticism of Kansas Governor Sam Brownback, including how easy it is to ignore inconvenient lessons of history.

-

No one is stealing* from KPERS

No one is stealing from KPERS, the Kansas Public Employees Retirement System. But there are related problems.

-

Year in Review: 2016

Here are highlights from Voice for Liberty for 2016. Was it a good year for the principles of individual liberty, limited government, economic freedom, and free markets in Wichita and Kansas?

-

Decoding Duane Goossen

The writing of Duane Goossen, a former Kansas budget director, requires decoding and explanation. This time, his vehicle is “Rise Up, Kansas.”

-

Kansas Governor Sam Brownback on myths and reality

Myth vs Reality: What the media isn’t telling you.

-

From Pachyderm: Radio Host Joseph Ashby

From the Wichita Pachyderm Club this week: Radio Host Joseph Ashby, host of The Joseph Ashby Show. His talk focused on the administration of Kansas Governor Sam Brownback.